Non-Performing Assets (NPAs) have become a massive worry for monetary foundations, controllers, and the economy in money and banking. NPAs address credits or advances that have stopped regularly producing pay for the moneylender because of default by the borrower. In this article, we’ll dive into NPAs, investigate their causes, examine their effect on monetary organizations and the economy, and discuss potential goal procedures. We are discussing Grasping Non-Performing Assets(NPAs): Causes, Effect, and Goal Techniques.

We are discussing Grasping Non-Performing Assets(NPAs): Causes, Effect, and Goal Techniques:

Characterizing NPAs

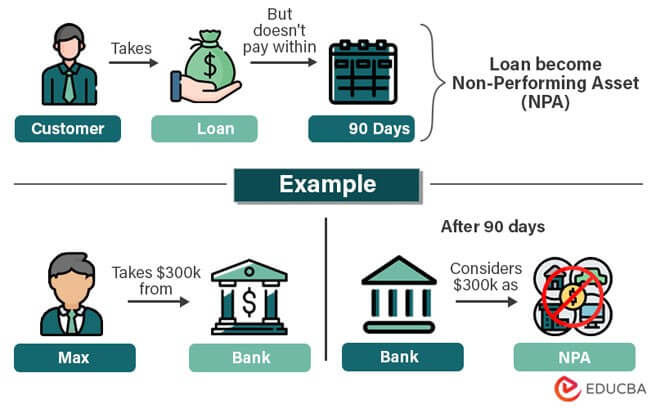

Non-performing assets (NPAs), or terrible credits or hindered resources, allude to credits or advances where the borrower has neglected to make planned installments of head and interest for a predetermined period, usually 90 days or more. When a credit turns into an NPA, it influences the moneylender’s monetary record as the standard pay from the advance turns dubious, and there’s a gamble of incomplete or complete loss of the chief sum.

Reasons for NPAs

A few variables add to the ascent of NPAs inside the financial area:

Economic Downturns

Financial downturns or slumps can prompt business disappointments, employment misfortunes, and diminished buyer spending, making it difficult for borrowers to reimburse their advances.

Ineffective Credit Assessment

A deficient reasonable level of effort and remiss credit appraisal cycles can bring about advances being reached to borrowers with frail credit profiles or questionable reimbursement limits.

Industry-Explicit Issues

Certain ventures, like foundation, land, and horticulture, are more inclined to NPAs because of task delays, market instability, and administrative difficulties.

Fraud and Stiff-necked Default

A few borrowers participate in fake exercises or tenaciously default on credits, which characterizes these credits as NPAs.

External Factors

Cataclysmic events, political precariousness, and worldwide occasions can unfavorably affect borrowers’ capacity to reimburse credits, adding to the ascent of NPAs.

Effect of NPAs

The expansion of NPAs can have sweeping outcomes on monetary organizations, the economy, and society:

Financial Institutions

NPAs dissolve banks’ and monetary organizations’ benefits and capital sufficiency. They tie up assets that could somehow be sent for useful loaning, turning off the organization’s capacity to help economic development.

Economic Growth

Elevated degrees of NPAs can smother credit stream to functional areas, hampering speculation, business venture, and occupation creation. This, thus, can hinder financial development and fuel poverty and imbalance.

Systemic Risks

The disease impact of NPAs can present foundational dangers to the monetary framework, particularly assuming numerous establishments are given to similar borrowers or areas. A far-reaching banking emergency set off by NPAs can have critical ramifications for the security of the whole monetary framework.

Investor Confidence

Rising NPAs can sabotage financial backer trust in the economic area and the more extensive economy, prompting capital flight, discounted venture inflows, and decreased resource costs.

Social Impact

The results of NPAs stretch past the monetary domain, influencing vocations, social attachment, and public confidence in foundations. Defaults on advances can prompt loss of work, resource seizures, and social agitation, especially among weak fragments of society.

Resolution Methodologies for NPAs

Resolving the issue of NPAs requires a multi-pronged methodology including monetary establishments, controllers, borrowers, and different partners:

Prudential Standards and Regulations

Controllers must authorize severe prudential standards and guidelines to guarantee mindful loaning rehearses, the substantial gamble of the executive’s structures, and reasonable acknowledgment and goal of NPAs.

Asset Quality Review (AQR)

Leading intermittent AQRs helps save money by distinguishing NPAs precisely and proactively addressing resource quality worries through provisioning, rebuilding, or recuperation measures.

Loan Recuperation Mechanisms

Monetary foundations can utilize different systems for NPA recuperation, including obligation rebuilding, resource adaptation, advance benefits, and lawful response through obligation recuperation councils or bankruptcy procedures.

Debt Rebuilding Schemes

States might present obligation-rebuilding plans or resource-remaking organizations to work with the goal of NPAs and alleviate borrowers confronting impermanent monetary misery.

Strengthening Corporate Governance

Further developing corporate administration rehearses inside monetary foundations can upgrade executives’ risk, straightforwardness, and responsibility, lessening the probability of NPAs emerging from remiss loaning principles or interior misrepresentation.

Promoting Monetary Inclusion

Improving admittance to credit for underserved sections of the populace, combined with monetary proficiency programs, can enable borrowers to pursue informed financial choices and lessen the rate of NPAs.

FAQs

What are Non-Performing Assets (NPAs)?

Non-performing assets (NPAs) are credits or advances that have quit producing pay for the loan specialist, generally because of default by the borrower. These credits are NPAs when the borrower neglects to make planned installments of head and interest for a predetermined period, typically 90 days or more.

Why are NPAs a worry for banks and monetary institutions?

NPAs represent a critical worry for banks and monetary foundations as they influence benefit, capital sufficiency, and, in general, financial well-being. NPAs tie up assets that could be conveyed for useful loaning, impeding the organization’s capacity to help monetary development.

What are the primary drivers of NPAs?

A few elements add to the ascent of NPAs, including monetary slumps, insufficient credit evaluation, industry-explicit issues, misrepresentation and determined default by borrowers, and outer factors like cataclysmic events and political instability.

What is the effect of NPAs on the economy?

Expanding NPAs can hamper financial development by smothering credit stream to functional areas, diminishing speculation, business, and occupation creation. Elevated degrees of NPAs likewise present foundational dangers to the monetary framework and subvert financial backer certainty, prompting capital flight and discounted resource costs.

How do banks and monetary foundations address the issue of NPAs?

Monetary establishments utilize different techniques to address NPAs, including reasonable provisioning, resource quality surveys, obligation rebuilding, resource adaptation, lawful plan of action through obligation recuperation courts or bankruptcy procedures, and fortifying corporate administration and hazard the board structures.

What job do controllers play in overseeing NPAs?

Controllers implement severe prudential standards and guidelines to guarantee mindful loaning rehearses, opportune acknowledgment, and goal of NPAs, and advance straightforwardness and responsibility inside the financial area. Controllers may present obligation rebuilding plans or resource reproduction organizations to work with NPA resolution.

How do NPAs influence borrowers?

Borrowers with NPAs face different results, including resource seizures, judicial actions, harm to financial soundness, and loss of admittance to credit. Defaults on advances can prompt social and economic difficulties, influencing occupations and intensifying poverty and disparity.

What steps could borrowers take at any point to keep away from NPAs?

Borrowers can relieve the gamble of NPAs by keeping a decent record as a consumer, sticking to credit reimbursement plans, speaking with loan specialists in the event of monetary troubles, investigating obligation rebuilding choices, and looking for economic guidance if necessary.

Are there any preventive means to diminish the rate of NPAs?

Preventive measures to diminish NPAs incorporate fortifying the gamble the executives work on, further developing credit evaluation systems, improving borrowers’ reasonable level of investment, advancing monetary proficiency and consideration, and encouraging a culture of mindful getting and loaning.

What are the drawn-out ramifications of a high NPA proportion for the financial area and the economy?

A high NPA proportion can dissolve financial backer trust in the economic area, lead to a credit crunch, and block monetary development. It can likewise strain monetary assets if state-run administrations are constrained to rescue battling monetary establishments, subverting financial manageability and long-haul advancement objectives.

Conclusion

Non-performing assets (NPAs) present considerable difficulties to the steadiness and strength of the financial area and the more extensive economy. Tending to the main drivers of NPAs requires coordinated endeavors from policymakers, controllers, monetary establishments, and borrowers. By executing reasonable loaning rehearses, compelling gamble the board structures, and ideal goal instruments, partners can moderate the unfriendly impacts of NPAs and cultivate a sound and feasible financial environment helpful for monetary development and monetary solidness. All partners must team up proactively and embrace an all-encompassing way to deal with and tackle the NPA issue and defend the drawn-out interests of contributors, financial backers, and society.